Getting the call from your insurer that your car has been written off is unsettling even when you were half expecting it. The car might still be sitting on your drive, might even still start, and yet you’re being told it’s a total loss. The letters and numbers that follow, Cat N, Cat S, sometimes still Cat C or Cat D if you’ve had this conversation before, don’t make it any clearer unless someone actually explains what they mean.

This guide walks through what a write-off actually is, what each category means in plain terms, what you’re legally allowed to do with your car afterwards, and how to decide whether repairing it or scrapping it makes more sense for you.

What Does “Written Off” Actually Mean?

A car is written off when an insurer decides that repairing it would cost more than the vehicle is worth, or more than a set percentage of its value, typically somewhere around 50 to 60 percent depending on the insurer. It doesn’t necessarily mean the car is a wreck. A relatively minor bump that damages an expensive sensor-packed bumper on a newer car can be enough to write it off, purely because the parts and labour cost more than the car itself is worth on paper.

Once an insurer decides to write a car off, they’ll usually offer you a cash settlement based on its pre-accident market value. What happens to the physical car after that depends entirely on which category it’s been assigned.

The Four Insurance Write-Off Categories

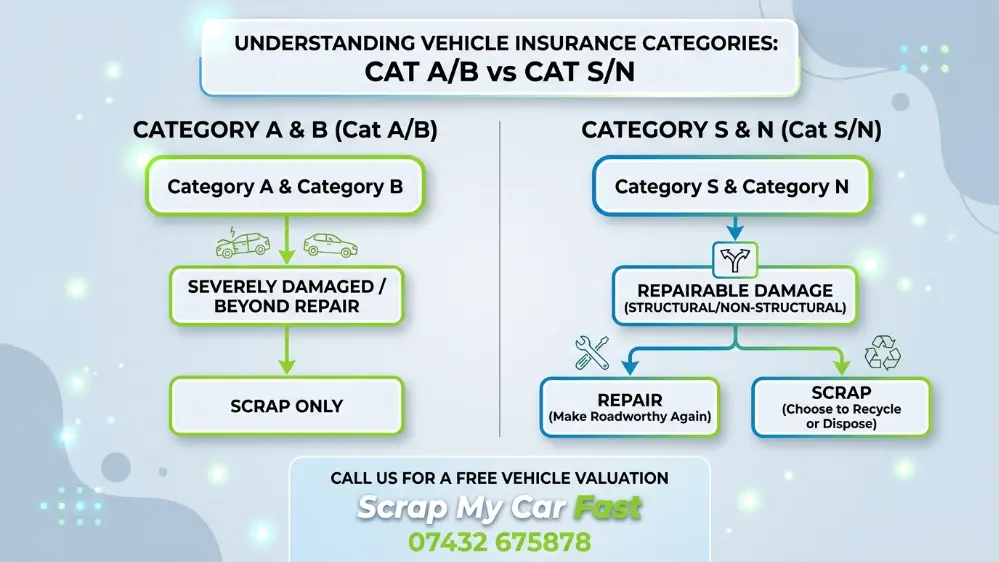

Since October 2017, the UK insurance industry uses four categories: Cat A, Cat B, Cat S, and Cat N. You’ll still hear people mention Cat C and Cat D, which were the older names for roughly the same ideas before the 2017 change, so if someone uses those terms they generally mean what we’d now call Cat S or Cat N.

Category A is the most severe. The car is so badly damaged that it must be crushed in its entirety. No parts can be salvaged or resold, and it can never be put back on the road under any circumstances.

Category B means the body shell must be destroyed and the car can never return to the road, but individual parts, the engine, gearbox, and other components, can be removed and sold on if they’re still usable.

Category S stands for structural damage. The car’s chassis or structural frame has been affected, but the vehicle can legally be repaired and driven again if it’s fixed properly. It’s the more serious of the two “repairable” categories, and it stays permanently marked on the vehicle’s history.

Category N stands for non-structural damage. This covers damage to things like bumpers, electrics, upholstery, or cosmetic panels, without any impact on the structural frame. These are the easiest write-offs to repair and get back on the road, though the write-off marker still stays on the car’s record forever, exactly the same as Cat S.

What Can You Legally Do With Each Category?

This is where people usually get caught out, because the rules are quite different depending on which letter your car has been given.

With a Cat A car, your only option is scrapping it through a licensed Authorised Treatment Facility for full destruction. There’s no legal route to keep it, repair it, or sell it on in any form.

With a Cat B car, the shell has to be destroyed, but you (or a breaker) can strip and sell usable parts first. Again, the car itself can never be re-registered or driven.

With a Cat S car, you can repair it and put it back on the road, but it’s worth doing this properly. A professional garage and, ideally, an engineer’s report documenting the repair will make life much easier if you ever want to sell it or reinsure it later. The Cat S marker never goes away, and future buyers or insurers will always see it.

With a Cat N car, you can also repair and drive it, and there’s no formal legal requirement for an engineer’s inspection the way there sometimes is with Cat S, though keeping receipts and photos of the repair is still a sensible habit. Cat N cars are generally easier to sell and insure afterwards than Cat S, simply because buyers see non-structural damage as less of a risk.

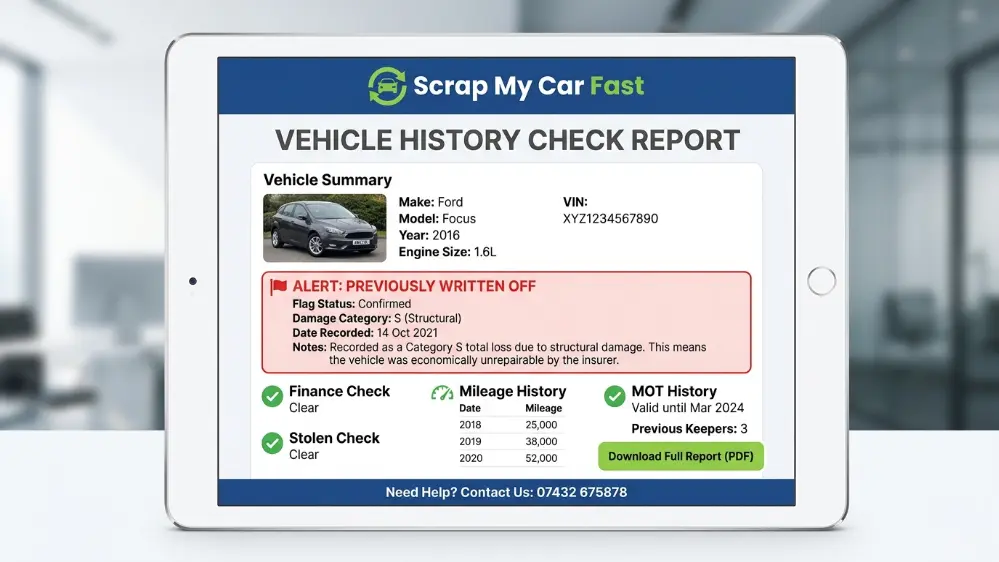

Does the Write-Off Marker Ever Disappear?

No. Once a car has a Cat S or Cat N marker on its history, that record is permanent. It’ll show up on any HPI check or vehicle history report for as long as the car exists, regardless of how well it’s repaired or how many owners it goes through afterwards. This is exactly why write-off history affects resale value even years later, and it’s worth being upfront about it if you do eventually sell the car privately.

How a Write-Off Affects Your Insurance Going Forward

It’s worth being realistic about this part too. Once a car has a Cat S or Cat N marker, it’s likely to cost a bit more to insure going forward compared with an identical car that’s never been written off, and some insurers will ask more questions or want to see repair documentation before they’ll cover it. This is a permanent feature of owning that vehicle, not something that fades after a year or two, and it’s a factor worth weighing up alongside the repair cost itself when you’re deciding whether keeping the car makes sense.

Getting a Second Opinion on the Settlement Figure

If the cash settlement your insurer offers feels low, you’re within your rights to push back on it, and it’s more common than people expect for insurers to revise a figure once challenged properly. The strongest approach is gathering three or four like-for-like listings for the same make, model, age, and mileage from sites like Autotrader, then presenting those directly to your insurer as evidence the valuation doesn’t reflect the real market. Insurers use trade guides for their initial figure, and those guides don’t always keep pace with what cars are actually selling for, particularly for older or less common models. It costs nothing to ask, and worst case, they simply confirm the original figure stands.

What Documents You’ll Need

Scrapping a written-off vehicle needs slightly more paperwork than a straightforward scrap job, simply because there’s an insurance claim tied to it. Alongside the usual V5C logbook and valid photo ID, it helps to have any letter or email from your insurer confirming the category assigned and the settlement details, particularly if you’re keeping the vehicle rather than letting the insurer collect it directly. If you’re unsure exactly what applies to your situation, our full FAQs page covers the most common paperwork questions we get asked, and our team can talk you through anything specific to your case before collection day.

What This Means If You’re Buying a Used Car

It’s worth flipping the perspective for a moment, because this same knowledge protects you as a buyer too. Always run a vehicle history check before buying any used car, since it will flag a Cat S or Cat N marker immediately, and a seller who fails to disclose write-off history when asked is misrepresenting the car, which gives you legal grounds to unwind the purchase. A properly repaired Cat N car with full documentation can still be a perfectly sound, safe vehicle to buy at the right price, but you should always be paying less for it than an equivalent car with no write-off history, and the seller should be upfront about it from the start.

Your Options After a Write-Off

Once you’ve had the category confirmed, you’ve got a handful of realistic paths forward.

You can accept the insurer’s cash settlement and let them take the vehicle, which is what happens automatically with most Cat A and Cat B write-offs. You can buy the salvage back from the insurer, usually at a reduced settlement figure, if it’s a Cat S or Cat N car you want to repair yourself. You can challenge the settlement figure if you think the valuation is too low, insurers will sometimes revise it if you provide solid evidence like comparable listings. Or, if you decide it’s genuinely not worth repairing, whether that’s a Cat S, Cat N, or any other damaged vehicle you’ve kept ownership of, you can scrap it for cash instead.

When Scrapping Makes More Sense Than Repairing

Repairing a Cat S or Cat N car only makes financial sense if the repair cost, plus the hit to resale value from the permanent write-off marker, still leaves you better off than scrapping it. For older cars, or ones where the damage touches expensive components like wiring looms, airbags, or sensor systems, that maths often doesn’t work out. If you’re staring down a repair quote that’s most of the car’s value, or you simply don’t want a permanently marked vehicle on your insurance going forward, scrapping it is usually the cleaner outcome.

We deal with written-off and accident-damaged vehicles regularly across Greater Manchester, and you don’t need the car to be driveable for us to collect it. If it’s been through an accident and the damage is significant, our scrap accident damaged car service covers exactly this, and if you’ve already got a category confirmed from your insurer, our sell written off car page walks through what we need from you to get moving. You can read more detail on how the local collection process works on our existing guide to scrapping a written-off car in Manchester, and whether you’re in the city centre, out in Stockport, or anywhere else across the ten boroughs, the same free collection and same-day payment terms apply.

What We Need From You

Whether it’s Cat S, Cat N, or a car that hasn’t been officially categorised but you know isn’t worth repairing, the process is the same one we use for any scrap my damaged car collection. You’ll need your V5C logbook if you still have it, though it’s not a legal requirement if it’s been lost, valid photo ID, and any insurance paperwork confirming the write-off category if one’s been assigned. Get an instant quote based on the vehicle’s details, and we’ll arrange free collection from wherever you’re based, whether that’s central Manchester or one of the surrounding boroughs.

Frequently Asked Questions

What’s the difference between Cat S and Cat N? Cat S means the car’s structural frame was damaged. Cat N means the damage was non-structural, things like bumpers, electrics, or interior. Both can legally be repaired and driven again, but Cat S is the more serious of the two.

Can I still drive a Cat N car? Yes, once it’s been properly repaired. There’s no legal requirement for a formal engineer’s report on a Cat N repair, though keeping evidence of the work done is sensible.

Do I have to tell my insurer if my car is Cat S or Cat N? Yes. When you insure a car with a write-off history, you’re legally required to declare it. Not doing so can invalidate your policy entirely.

Can you scrap a Cat A or Cat B car for cash? Cat A and Cat B write-offs are usually taken directly by the insurer for destruction as part of the settlement, so you won’t typically have the option to scrap it yourself for extra cash. If you do retain ownership, a licensed ATF can still process it, but the vehicle must go through full destruction and can never be resold as a runner.

Will a Cat S car be worth less if I sell it later? Yes, almost always. The permanent write-off marker means buyers and future insurers will always see the car’s history, and this typically knocks a noticeable amount off resale value even after a proper repair.

Can I challenge my insurer’s write-off valuation? Yes. If you think the settlement figure is too low, gathering evidence of comparable cars for sale and presenting it to your insurer can lead to a revised offer. It’s a straightforward conversation to have and costs nothing to try.

If you’ve decided repairing isn’t worth it, get your instant quote today and we’ll take care of the collection, paperwork, and same-day payment.